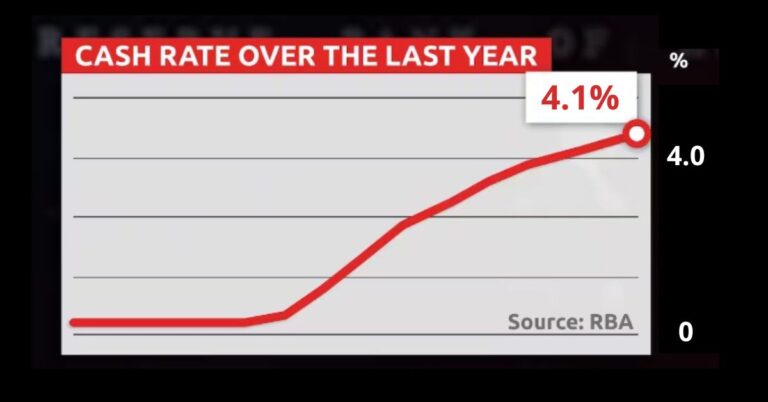

Most people have been dealt another shit sandwich this month, with interest rates going up again. I don’t know about you, but I’ve never actually eaten a shit sandwich…

But I do have a sneaky suspicion it tastes something like this:

Rising living expenses are adding to this bad taste.

For a simple way to find an extra $50-100 per week, I’ve developed this mashed up version of a lot of books and other resources I’ve read on this topic over the years.

Most people prefer to complain about their money on external things they can’t control. It’s easier than rolling your sleeves up for about 1-2 hours of work in structuring your finances and then leave it on autopilot.

It’s not a budget, that’s a dirty word for some. It’s an automated personal finance system. It really is like getting free money.

Even if you don’t need the extra money, this system creates a feeling of freedom and less stress about managing your finances and instantly creates extra cashflow.

I tried to inject some fun and a few laughs with it, and I still sometimes ask my girlfriend how much pocket money I have.

But the most important thing – you still get whatever you want, but without the stress, worry or brain-clutter that comes with managing your personal finances. I have an account called “whatever i want” and that gets more than enough money every month for me to go bananas if I want to.

Here’s a screenshot of my actual internet banking:

Explanation of Recommended Bank Accounts

See the full article of how to create a Personal Finance System over here.

| Bank Account 'label' | How to use your account |

|---|---|

| Base Camp | It's called Base Camp, because everything passes through here. It is the central hub of your finances, where all income is deposited. This account should not be used for external transactions or payments. Instead, it should be used to feed other accounts that you create for specific purposes, such as bills, groceries, and discretionary spending. It is important to limit access to this account and ensure that cash is not withdrawn from any other source. One way to do this is by not allowing ATM card access to the Base Camp account. |

| Pocket Money | To better manage your daily spending, create a separate account specifically for expenses associated with your normal daily activities. This can include things like recreational activities, haircuts, takeout food, dining out, and fuel. Be sure to exclude any expenses that could be allocated to household or grocery items. Make this account your primary savings account on your ATM card for easy access, or get a separate Visa Debit. This can help you track your spending and stay within a budget for daily expenses. Tips: • Use cash for daily spending activities and withdraw it from this account. • Set a weekly budget that is slightly less than your previous spending habits. • Regularly transfer a weekly cashflow to this account to help reduce spending and promote awareness of expenses. • The frequent replenishment of funds also creates a natural process of delaying unnecessary discretionary spending. |

| Groceries | For regular groceries and items you take home (excludes alcohol, which comes from the Pocket Money account). Tips: • Set a weekly budget that is slightly uncomfortable, but not overly restrictive, to encourage more affordable eating at home (eg. 10% less than previous spending habits). • Adopt a simple rule: food bought and taken home comes from the Groceries account, while eating out expenses come from the Pocket Money account. This helps distinguish between necessary expenses and discretionary spending. • Use a separate Visa Debit or ATM card solely for regular groceries and items you take home (excluding alcohol). |

| Bills | Include every bill you need to pay regularly. Such as monthly direct debits, loan repayments, insurances, Netflix, etc. Tips: • Set up utilities to be auto direct debited every fortnight or month, which may lead to a slight overpayment that you can retain as a credit on your account. • Calculate the total monthly amount required and ensure that every time you’re paid, you immediately credit the bills account with the required amount (plus an extra $50 per month, which builds a surplus to cover unexpected increases in utilities and other usage accounts). This approach saves a lot of time and reduces stress associated with managing these items. |

| Whatever | Your "whatever i want" takes away the restrictions and thoughts of 'going without' many associate with having a budget, and is for any discretionary purchases or expenses, such as recreation, shopping, hobbies, and online purchases. It can also serve as a backup source of funds in case one of your other accounts is running low on cash. |

| Safe | Your "safe" (savings) account is specifically designed for long-term savings and is not recommended for short-term goals such as holidays or purchases. Tips: • Create a savings goal that’s meaningful to you, and feels good when you see it build up after several pay periods consecutively. • If you have a specific additional purpose in mind, such as a holiday, it’s better to set up another account for that purpose. • This account should not be linked to your ATM card, to avoid any temptation to use the money for other purposes. |

| Other | Create further accounts for purposes that suit your lifestyle, such as “holiday” account, “children” account. |

FFS, enter your real details to get the weekly tips

Articles and other things I thought you’d like because you’re interested in some things sometimes…

ANZ Says Interest Rates To Rise Another 0.5% By August

After the latest job number released this week, ANZ expecting some more immediate rate rises as per this article.

The RBA Bulletin 15/06/2023

Published yesterday by the RBA includes a lot of interesting insights to the Rental Market, and several other categories you might be interested in. Go to the RBA Bulletin here.

Causes of Inflation

Interestingly, inflation expectations can actually influence inflation. One of the factors mentioned in this article by the RBA talks about how ‘Inflation Psychology’ can contribute to a higher rate of actual inflation. So expectations about inflation become a self-fulfilling prophecy.

Useless Financial Information

Tulip Mania was the first known/reported ‘speculative financial bubble’ in the 1600’s. It’s totally insane how high the prices went for a plant bulb. According to wikipedia several tonnes of food, beer, wine, 12 sheep, 8 fat swine, and several other items of value were trading for a single tulip bulb.

Stoic quote I think a lot about

“We must give up many things to which we are addicted, considering them to be good. For greatness of the soul will be lost, which can’t stand out unless it disdains as petty what the mob regards as most desirable.” – Seneca.

I’ve read this quote about 1000 times. For me, this quote is about a deep inward journey to learn more about yourself. Identifying habits that work for you and your goals, or against them. For me, understanding myself more and removing habits that were not helpful or were from the outside world, has actually helped me develop deeper relationships.

Important Economic Announcements from this week

Some of this could impact RBA’s decision to increase rates again soon…

Unemployment down to 3.6%, after being at 3.7% last month

Full employment increased by 61.7K, after a 28.6K reduction last month

Consumer sentiment increased 0.2% (higher than expected), after being down 7.9% previous month

promo

Next week

How you can earn money while you sleep, with the flick of this one little switch (hint: it’s nothing to do with work, investing, or doing anything at all really)

Other topics Coming Soon

Debt Reduction Strategies: How to pay off your home loan faster

Business owners can access 100% of property value without interest loadings

Simple way to determine your purchasing power

Compare Max Loans: Bank A $100K, Bank B $1.5M, exact same financial data